Women And Finance

2024/10/03

2024/10/03

The ability to manage money efficiently and effectively requires time and practice, irrespective of gender. In India almost half of the population are women. So, their empowerment and not just financial literacy but adequacy to take leadership is key to the socio-economic growth of the country.

DBS bank in collaboration with CRISIL has produced the third report in its “Women and Finance” series. The report provides insights into the sources of business funding, banking habits, digital payment preferences, adoption of sustainability measures and workforce dynamics. Additionally, the report also focuses on gender-specific challenges of women entrepreneurs considering factors like age, income level and geographical location; and how these factors influence their decisions. The report also provides insights into the areas in which women entrepreneurs seek support. The earlier two instalments were released in January and March of 2024. The first one explored savings, investment patterns and behaviours among women entrepreneurs while the second one delved into career progression, workplace policy preferences and challenges faced by women in the workforce.

The report employs the triangulation method, a mixture of quantitative as well as qualitative study. It focuses on 400 working urban women living across 10 major cities in India. 250 of them were subjected to robust face-to-face interpersonal conversations for quantitative data. The rest 150 were part of a focused group discussion to gather qualitative insights.

The age group of the women entrepreneurs were categorized into three categories. 29% of the respondents were 25-35 years old, 46% of the respondents were 36-45 years, and 15% of the respondents were more than 45 years old. 34% belonged to semi-affluent with yearly income ranging from 10-15 Lakhs, while 43% emerging affluent with yearly income ranging from 26-40 lakhs, and 23% affluent with yearly income ranging from 41-55 lakhs. While marital status of the respondents included four categories 4% unmarried without any family members, 7% unmarried with other members dependent on them, 23% unmarried without any dependent family members, and 66% married with at least one family member dependent on them.

The classification of these categories is important as people belonging to affluent families usually have a better understanding of personal and corporate finance, while less affluent people struggle with investments, personal savings and funding enterprises. While those who have family members depending on their income tend to be more unstable with loans and savings. All individual’s financial choices are the result of multiple factors. It is to be noted that correlation between two factors does not imply causation.

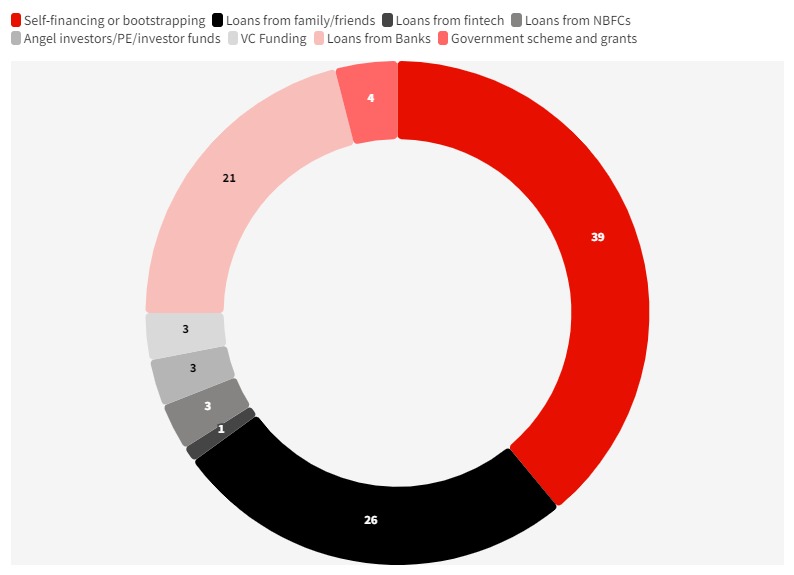

Self-financing is the most popular choice among women looking to fund their business, followed by loans from family and friends and bank loans. Minute percentage of women entrepreneurs look at NBFC, Angel Investor, PE etc. Whereas fintech companies are the least popular funding choice.

The reliance on personal funds for business operations increases with age. 52% of women over the age of 45 use their savings to fund their business, whereas 37% between the age group 36-45 and 36% between the age group 25-35 use self-financing to fund their business.

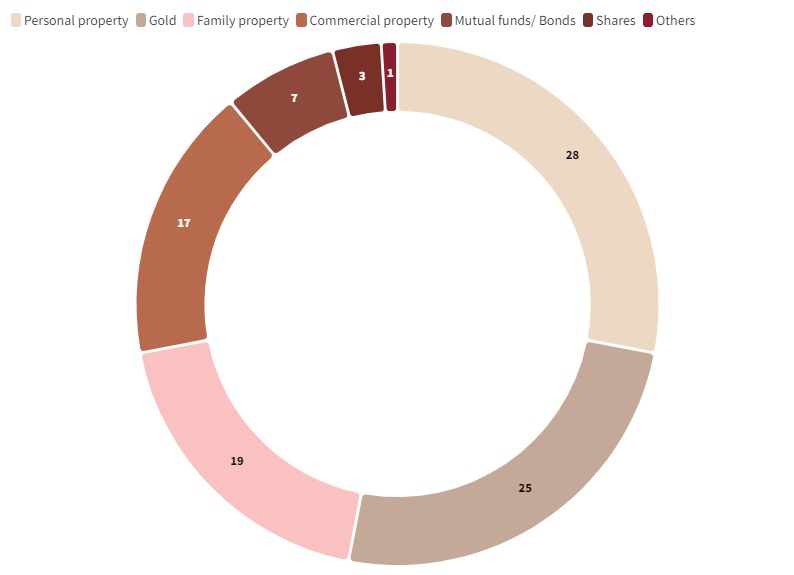

Personal property and gold are the top choices as collateral to secure a loan. This is followed by family property, commercial property, mutual funds/bonds, shares and others. Only 3% of women entrepreneurs use mutual fund shares as collateral. This depicts the risk-averse approach.

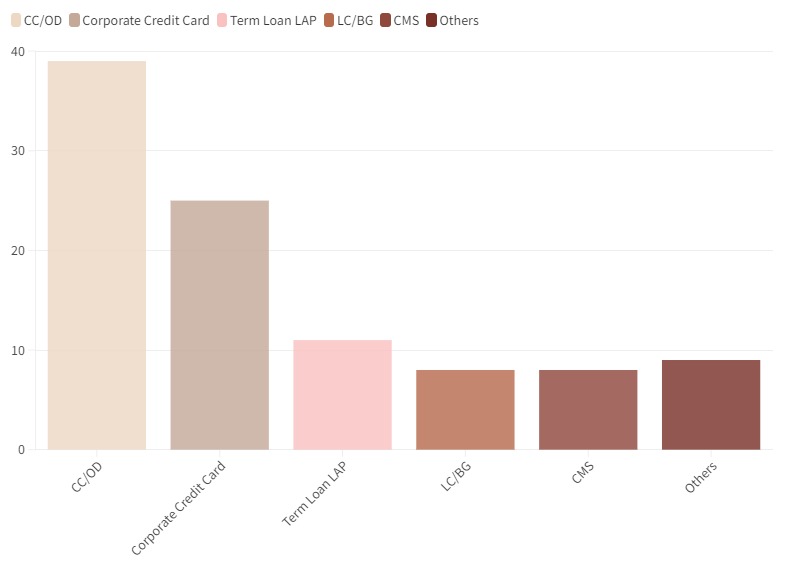

39% of women entrepreneurs prefer cash credit/ overdraft facilities, followed by Corporate Credit Cards by 25% of women, 11% of women prefer term loans, 8% of self-employed women prefer a letter of credit/ bank guarantee, another 8% prefer cash management system, while others 8% prefer supply chain finance, pre-shipment and post-shipment finances.

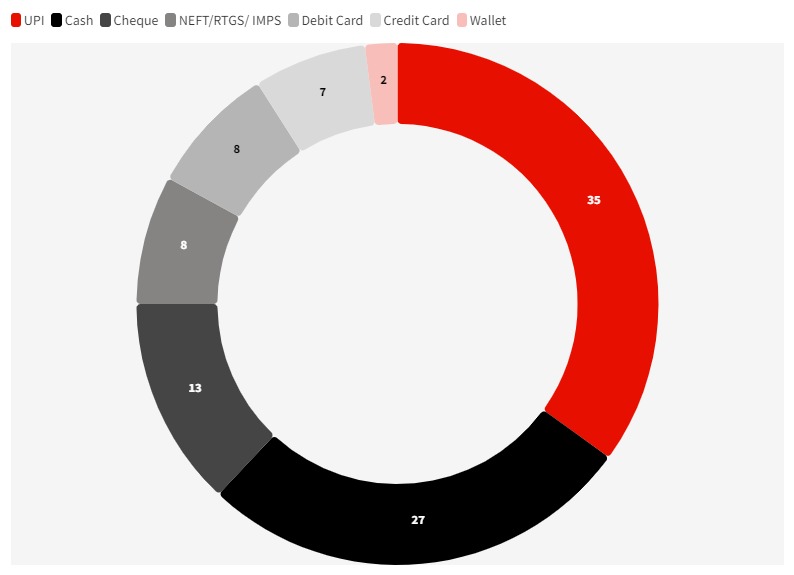

73% of self-employed women surveyed as part of the study preferred receiving payments from customers digitally, and 87% used digital methods to pay their business expenses. UPI is the most-used mode for both receiving (35%) and paying (26%) business expenses. However, cash remains indispensable for payroll and operational expenses, used by 36% of respondents

UPI has played a major role in the digitalization of India’s financial transactions, According to RBI, the share of UPI in digital payments has reached close to 80% in the fiscal year 2024. Delhi, Pune and Hyderabad are leading the digital payment adoption drive for businesses. 97% of self-employed women in Delhi use digital modes for business payments, followed by Hyderabad 93%, Mumbai 90%, Bengaluru 79%, and Kolkata 64%.

The usage of cash is predominant for payroll and employee expenses. Credit and Debit cards are mostly used in travel bookings. Net banking sees higher usage in operational and payroll expenses. Wallets are mostly used for e-commerce payments.

A 27-year-old self-employed woman in Kolkata stated, "UPI is widely accepted by vendors these days, and we can use 11% screenshots as proof. The rewards and cashback offered with UPI are some of the added benefits.Among self-employed women Kolkata ranks lowest in gender bias stands at 0%. Whereas in the South it is highest with 33% of respondents in Bengaluru perceiving gender bias while interacting with vendors and networking with peers. Pune comes next with 28%, followed by Delhi 11%. The all-India average is 16%. These biases occur while networking with peers, clients, and industry bodies, raising funds or financing their businesses, and interacting with various vendors. While dealing with vendors shows the highest bias of 20%, dealing with bank records lowest of 2%. Other notable instances of bias occur while networking with peers, clients and industry bodies (18%), procuring orders from clients (16%), fundraising and financing (15%), dealing with family’s apprehension towards business (18%), recruiting/ hiring talent (10%).

“Some of my clients underestimate my competence because I am a woman. Instead of sharing their queries with me, they want to talk to my male employees,” said a 28-year-old self-employed woman in Pune.A majority of 29% of respondents manage all aspects of their business. In contrast, only 7% of women are involved in HR- management which is traditionally dominated by women. 37% of respondents select more than 40% of women employees for their team. 66% of respondents are actively contributing towards their retirement plans. Whereas only 38% offer those benefits to their employees.

Delhi leads in providing retirement benefits with 68%, followed by Bengaluru at 58%, Mumbai at 33% and Kolkata at its lowest with 3%.

“I have less than 20 employees, so offering a provident fund is not mandatory. However, I choose to offer it as part of my employees' retirement plan," said a 32-year-old self-employed woman from Kolkata

2024/07/17